Via S&P Global Platts Insight blog,

A look at crude oil quality across countries that have committed to cutting production, tumbling global gas prices, and trends in steelmaking raw materials all feature in this week’s pick of visuals.

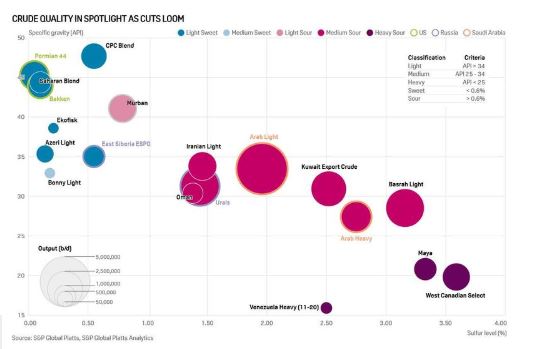

1. As OPEC+ agreement kicks in, heavier crude could see bulk of cuts

What’s happening? The OPEC+ production cuts go into effect May 1, and the beleaguered oil market will be watching to see if the 23-country alliance led by Saudi Arabia and Russia fulfills its commitment to rein in 9.7 million b/d of crude output.

What’s next? The market will also be counting on economically forced shut-ins by other key producers, such as the US and Canada, to bring global supply down in line with coronavirus-hit demand. Crudes towards the heavier end of the quality spectrum are likely to see the bulk of OPEC+ cuts, though the coalition produces grades of all qualities.

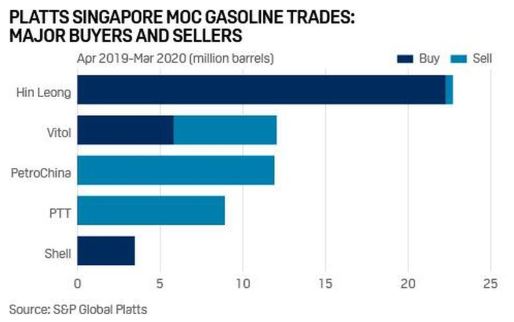

2. Singapore oil trader’s bankruptcy stuns bunker, storage sectors

What’s happening? Hin Leong Trading’s financial crisis is likely one of the world’s biggest bankruptcies in oil trading and the most significant after this year’s historic oil price crash. It has shunted Singapore’s bunker and oil storage sectors into uncertainty, with banks heard to be tightening credit to many players. Bunker suppliers including Minerva Bunkering and TFG Marine, who were both awarded bunker licenses recently, are expected to fill the supply gap. Gasoline has also been affected. Overall, the company’s trades represented 55% of total gasoline trades during the Platts MOC process between April 2019 and March 2020. Rivals like Saudi Aramco and Petronas are likely to fight for market share after HLT’s ouster.

What’s next? Market participants will be monitoring developments, to determine if the possibility of HLT’s successful restructure exists, while keeping an eye on commodity prices to asses if they stay supported, reflecting the supply shock created by the situation. The HLT debacle has also sparked opportunities for further consolidation in the Singapore market, with several suitors including Sinopec heard to be interested in acquiring assets of the beleaguered company.

3. Gas prices, margins plunge as coronavirus slashes global demand

What’s happening? Global gas prices continue to converge around record lows, with prices in the US, Europe and northeast Asia all now trading at or below the $2/MMBtu mark. The coronavirus outbreak has hit global gas demand hard, impacting a market that was already reeling from the mild northern hemisphere winter, record high gas stocks and continued oversupply.

What’s next? The JKM, TTF, and Henry Hub prices are now essentially interchangeable which is fully compromising any arbitrage. Market players are seeing only tiny margins from trading gas, and with storage sites filling quickly, prices could still have room to fall further as the summer progresses. Producers are feeling the pinch and industry is watching closely for signs of further supply curtailments in the coming weeks.

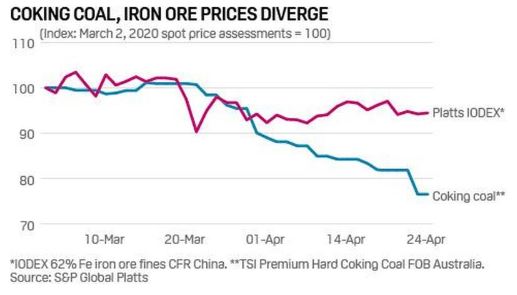

4. Coking coal prices fall as faltering economies pressure steel demand outside China

What’s happening? Coking coal prices have weakened through April toward $120/mt FOB Australia, as global steel output fell from the economic fallout of the coronavirus pandemic. European, Indian and US steel mills suddenly reduced demand for coke, the processed form of coking coal, in Q2. Steel output is expected to fall significantly this year, based on company plans. China’s dependence on iron ore imports, along with production disruptions in Brazil, South Africa, India and Canada, kept spot prices of the product relatively steady. China has maintained strong steel production so far this year, with pig iron rates growing in the first quarter on 2019.

What’s next? The decline in benchmark coking coal prices to the lowest in almost four years is leading mines to be idled, especially in the US, as higher cost production squeezes mine margins. Demand may fall longer term, as environmental controls continue to challenge permitting for new and existing steel and coke operations. Coke plants in Europe and Japan have idled with plans for permanent closures. Steel margins globally remain weak, which could slow restarts of idled steelmaking plants in the US, Europe and India, with longer-term potential for greater use of scrap and direct reduction iron.

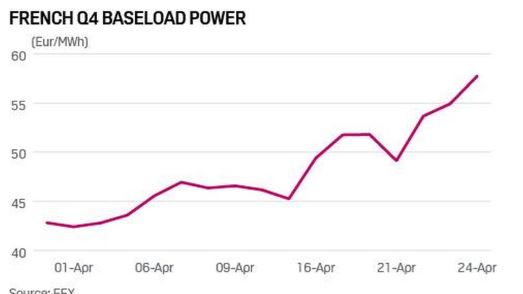

5. French winter power rallies as nuclear cuts outweigh demand losses

What’s happening? French Q4 2020 power prices rose over 30% after the country’s dominant generator utility EDF detailed nuclear reactor shutdowns due to the coronavirus crisis. Restrictions on movement are impacting summer maintenance and refueling across the nuclear fleet in France, with many reactors now unable to refuel before the winter. This has forced EDF to shut some units now to preserve fuel ahead of winter, with a knock-on impact stretching deep into 2021.

What’s next? A return to anything near normal electricity demand in the second half of the year would leave a significant cut in supply from nuclear, with the final quarter of 2020 most at risk of a capacity squeeze during cold snaps, when French electric heating demand spikes. Gas and modern coal units in France and across its borders would be called on to fill any “thermal gap” in supply, which opens as cheaper nuclear, renewables and hydro sources fail to meet demand. Increase fossil generation would in turn increase demand for European carbon allowances, this offering further support to near-term power prices.